.png)

Year End Tax Preparation: Avoid Common Filing Mistakes

Key Highlights

Here's a quick look at what you need for a smooth tax season.

- Understand that your fiscal year end doesn't have to be December 31st.

- Use a detailed tax preparation checklist to gather all your financial statements.

- Clean up your bookkeeping records to ensure accurate cash flow tracking.

- Maximize your tax return by identifying all eligible tax credits and deductions.

- Avoid common mistakes like missing deadlines or filing incomplete forms.

- Start your preparations early to make the end of the tax year less stressful.

Introduction

As your business year comes to a close, your focus shifts to year-end tax preparation.

Working with a professional tax service like Ma tax can make this process smoother, ensuring you meet all CRA requirements while gaining valuable financial insights.

This process is more than just a task; it's a critical step in meeting your tax obligations with the Canada Revenue Agency (CRA) and gaining valuable insights into your company’s financial performance.

Being organized and proactive can transform tax time from a stressful scramble into a calm and confident process.

This guide will walk you through preparing your tax return and avoiding common mistakes.

Essential Steps for Year End Tax Preparation in Canada

Getting ready for tax time involves more than just filling out tax forms. A solid strategy starts months before your filing deadline.

Creating a comprehensive tax preparation checklist is one of the most effective ways to stay organized and ensure you don’t miss a thing.

This involves understanding your fiscal year, knowing your corporate income tax deadlines, and keeping your records in order.

Let's explore the foundational steps you need to take to prepare for filing your tax return.

.png)

Determining Your Fiscal Year End for Tax Purposes

Did you know that in Canada, your company's fiscal year end doesn't automatically on December 31st?

Corporations have the flexibility to choose any year-end date, as long as it's within 53 weeks of their incorporation date.

Many businesses align their tax year with the calendar year for simplicity, while others choose a date that corresponds with their industry's slow season to better manage reporting and cash flow.

Once you select a date, it becomes your consistent fiscal year end.

The Canada Revenue Agency (CRA) expects you to use the same effective date each year. Changing this date is possible but requires official approval from the CRA.

If you decide to change your fiscal year end, you may need to file a return for a shorter period, known as a "stub period." Keeping accurate financial records throughout this process is crucial for a smooth transition.

CRA Year End Requirements Every Business Needs to Know

Meeting your tax obligations with the CRA means understanding and adhering to key deadlines.

For Canadian corporations, the timeline for your corporate income tax is a two-step process that you must manage carefully to avoid penalties.

Your tax payment is due sooner than your filing. Payments are typically due within three months after your fiscal year end.

Your corporate tax return, or T2, must be filed within six months of your year-end.

For example, if your year-end is December 31, your payment deadline is March 31, and your filing deadline is June 30.

Beyond deadlines, the CRA has specific requirements for record-keeping and compliance. Here are a few key points:

- Maintain accurate financial records for at least six years.

- Ensure all GST/HST remittances are up-to-date.

- Confirm payroll reporting and remittances are compliant.

- Pay your tax balance on time, even if you file your return later. Working with professional tax services can help ensure your filing process is seamless during tax season.

Bookkeeping for Year End: Setting Up Your Records

Clean and organized bookkeeping is the foundation of a stress-free tax season.

Before you can even think about filing, your financial records need to be in perfect order.

A reliable accounting system ensures your cash flow is accurately tracked and all transactions are accounted for.

If bookkeeping feels overwhelming, Ma tax offers professional bookkeeping and payroll preparation services to help you stay organized and compliant before tax season.

This process involves a thorough reconciliation of your accounts and a final review to close your books for the year.

By taking these steps, you create a clear and accurate picture of your business's financial health.

Let's look at how to close your books and reconcile your accounts properly.

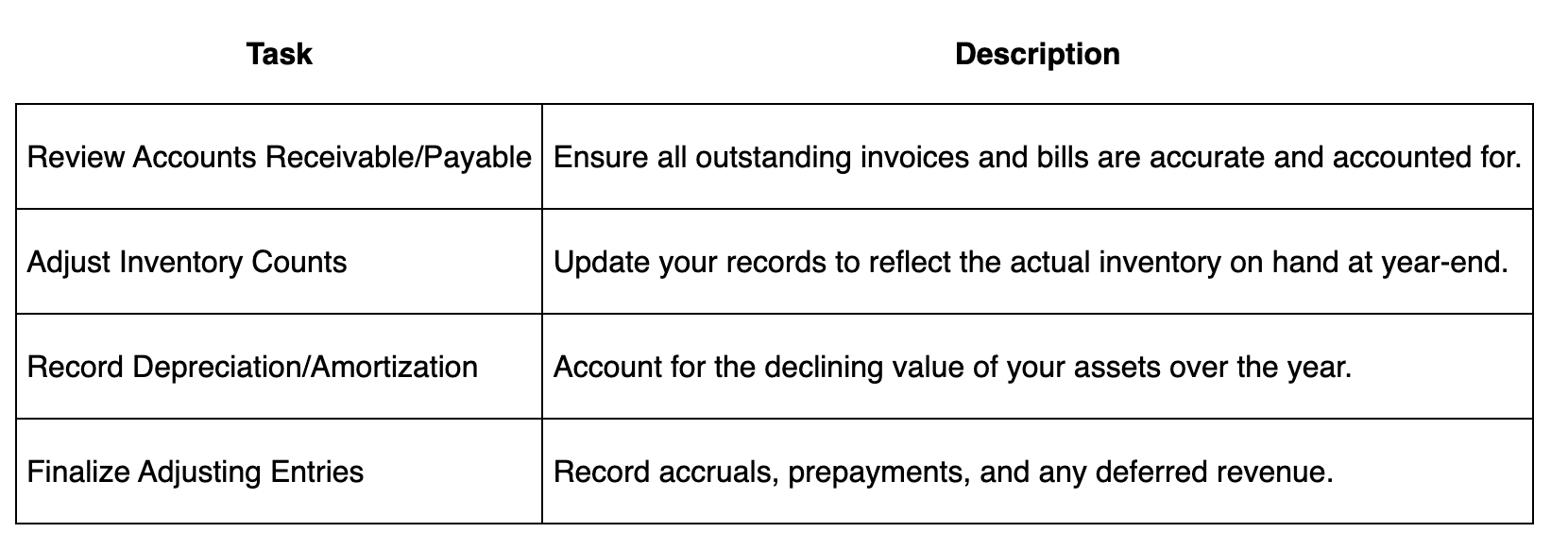

Closing Out Your Accounting Books Accurately

The annual close of your accounting books is a critical step in preparing for tax time.

This process ensures that your financial statements, like your balance sheet, accurately reflect your company's performance for the year.

Think of it as a final cleanup of your general ledger before passing your records to an accountant.

This involves reviewing all your business accounts, ensuring income and expense entries are current, and making necessary year-end adjustments.

These adjustments can include recording depreciation, prepayments, and accruals. Getting this right is key to understanding your true financial health.

An effective accounting system simplifies this process. Here are some of the key tasks involved in closing your books:

Reconciling Bank Accounts and Financial Statements

Reconciliation is the process of matching the transactions in your books to your bank statements and credit card statements.

This step is essential for catching errors, identifying discrepancies, and ensuring every dollar is accounted for.

Before closing your books, you must complete a thorough reconciliation for all bank and credit accounts.

Once your accounts are reconciled, you can finalize your key financial statements.

These documents are not just for tax filing; they provide deep insights into your business's performance.

Reviewing them helps you identify profitability trends, find areas for cost reduction, and plan your tax payment strategy.

Your year-end financial statements package should include:

- Income Statement: Shows your profit and loss over the fiscal year.

- Balance Sheet: Provides a snapshot of your assets, liabilities, and equity.

- Cash Flow Statement: Tracks the movement of cash in and out of your business.

Gathering Important Documents for Corporate Year End Taxes

With your books cleaned up, the next step is to gather all the necessary documents for filing.

The CRA requires detailed records to support the claims you make on your tax forms.

Having everything organized in one place will save you and your accountant significant time and ensure accuracy.

Using a tax preparation checklist is the best way to make sure you don't miss anything.

For tax purposes, this includes everything from income records and expense receipts to payroll files and investment statements.

Let's break down the specific documentation you'll need.

Income, Expense, and Payroll Documentation

Your core business records form the backbone of your tax filing.

These documents provide a detailed account of your business income and spending activities throughout the year.

It's vital to have comprehensive and organized financial reports ready for your accountant.

If you have employees or work with subcontractors, your payroll taxes and related documentation are just as important.

The CRA has strict rules for reporting payments to others, and having these records in order is non-negotiable.

Using any carry-forward amounts from a previous loss statement also requires proper documentation.

Here is a list of essential business documents to gather:

- Sales invoices, receipts, and bank deposit slips

- Contracts and loan agreements with year-end balances

- T4SUM (Summary of Remuneration Paid) for employees

- T5013 (Partnership Information Return) if you are in a partnership

- T5018 (Statement of Contract Payments) for construction subcontractors

.png)

Supporting Receipts and Tax Slips Required by the CRA

The Canada Revenue Agency requires you to keep supporting receipts for all the business expenses you claim.

This applies whether you operate as a corporation or as one of the many sole proprietorships in the country.

Digital copies are acceptable, which can make organizing them much easier.

In addition to receipts, you need to collect all relevant tax slips.

These slips report various types of income and contributions made throughout the year.

Forgetting to include a tax slip is a common mistake that can lead to reassessments and penalties.

Be sure to gather the following tax slips and personal receipts:

- T4 slips for employment income

- T4A and T5 slips for other income, such as from pensions or investments

- RRSP contribution slips

- Receipts for eligible charitable donations and medical expenses

- Tuition or educational expense receipts

Maximizing Deductions with Year End Accounting Tips

One of the most important goals for small or medium business owners at tax time is to lower their taxable income legally.

This is achieved by claiming all eligible business expenses and tax credits. Proactive year-end planning can uncover significant opportunities to reduce your tax bill.

From claiming capital cost allowance (CCA) on your assets to prepaying eligible expenses, the right strategies can make a big difference to your tax return.

Let’s explore some of the key deductions and write-offs you should be aware of.

Eligible Small Business Tax Credits and Write-Offs

Identifying every possible tax write-off is key to improving your company's financial health.

Many small and medium business owners are surprised to learn how many of their day-to-day costs qualify as deductible business expenses.

Keeping detailed records throughout the year will help you maximize your claims and reduce your business income tax.

Beyond standard expenses, look into specific tax credits available to your business.

These can include incentives for research and development (SR&ED), job creation, or digital media.

A small or medium business tax preparation checklist can help you track these opportunities so nothing gets missed on your tax return.

Common write-offs include:

- Advertising and marketing costs

- Insurance premiums, business taxes, and membership fees

- Legal and accounting fees

- Interest and bank charges

Work-From-Home and Business Expense Deductions

If you use a portion of your home for your business, you may be able to claim home office expenses.

This deduction is based on the percentage of your home dedicated to business use.

You can claim a portion of costs like rent, utilities, insurance, and property taxes.

Similarly, if you use your personal vehicle for business purposes, you can deduct related vehicle expenses.

It is crucial to keep a detailed logbook of your business mileage to support your claims. Proper tracking today can significantly impact your tax situation for the next year.

Eligible work-from-home and vehicle expenses often include:

- A portion of rent or mortgage interest

- Heating, electricity, and home insurance costs

- Fuel, oil, and maintenance for your vehicle

- Vehicle insurance and registration fees

- Leasing costs and business-only parking fees

Common Tax Filing Mistakes to Avoid

Even with the best intentions, mistakes can happen during tax filing.

That’s why many small and medium business owners rely on Ma tax for accurate, stress-free year-end tax preparation.

These errors can lead to delays, penalties, or even a CRA audit.

Knowing the common pitfalls is the first step to avoiding them and ensuring a smooth filing process for your tax return.

From missing important deadlines to filing with incomplete information, these mistakes are often preventable with careful planning.

Working with a professional tax preparer or tax advisor can also provide a safety net. Let's cover two of the biggest mistakes to watch out for.

Overlooking Deadlines and Filing Incomplete Forms

Missing deadlines is one of the most costly and easily avoidable tax mistakes.

The CRA imposes strict penalties and interest on late filings and payments, so marking your calendar with the correct dates is essential to meeting your tax obligations.

For corporations, your tax payment is due within three months of your fiscal year-end, while the filing itself is due within six months.

Self-employed individuals must pay any taxes owed by April 30th and file their return by June 15th.

Filing incomplete tax forms is another major error.

This can happen if you forget to include a slip, a schedule, or information from a previous loss statement.

To avoid these mistakes:

- Start your filing process early.

- Double-check that all tax forms are complete.

- Confirm all income slips have been included.

- Pay your tax balance on time, even if you file later.

Not Consulting a Tax Accountant Toronto for Guidance

Many business owners believe they can handle their taxes alone with online software.

While this is an option, a professional tax advisor does more than just prepare and file your return.

They act as a long-term partner, offering guidance on major financial decisions and their tax implications throughout the year.

A good tax accountant in Toronto should be available to answer your calls and emails year-round, not just during tax season.

They can provide peace of mind by ensuring your filings are accurate, optimized, and compliant.

This level of support is invaluable for busy business owners who want to focus on growth.

A professional offers a range of tax services, including:

- Optimizing your tax return to maximize savings.

- Providing accurate tax advice for your long-term plan.

- Ensuring you are compliant with the latest tax laws.

- Representing you in case of a CRA audit.

.png)

Conclusion

In conclusion, year-end tax preparation is a vital process that requires careful attention to detail to avoid common pitfalls.

By understanding the essential steps and gathering the necessary documentation, you can ensure that your filings are accurate and complete.

Additionally, staying informed about potential deductions and consulting with a tax professional can significantly enhance your financial outcome.

Don’t let year-end taxes become a last-minute hassle.

Contact Ma tax today for professional tax filing, bookkeeping, and payroll preparation services across Toronto and the GTA.

Frequently Asked Questions

What is the deadline for filing year end corporate tax returns in Canada?

In Canada, the deadline for filing your T2 corporate tax return is six months after your company's fiscal year end. However, the Canada Revenue Agency requires you to pay any taxes owed within three months of your fiscal year end. Missing these deadlines during tax season can result in penalties.

How does year end tax preparation differ for sole proprietors versus incorporated businesses?

The tax preparation process varies significantly. Sole proprietors report their business income and expenses on Form T2125, which is part of their personal income tax return (T1). Incorporated businesses are separate legal entities and must file a standalone corporate tax return (T2), which has different tax obligations and deadlines.

Where can I find professional resources for tax preparation in Toronto?

For business owners in Toronto, local firms like MA Tax Inc. in Scarborough offer expert tax services. Consulting a professional tax accountant in Toronto or a qualified tax preparer can provide you with personalized guidance. A tax advisor ensures your business stays compliant and helps you optimize your financial strategy.